Estate Deductions Subject To 2 Floor

Checklist Of Documents Required For Filing Tax Return Of Salaried Person Download This Checklist From Https Taxdosti Com Filing Taxes Tax Return Informative

Notice Of Late Rent Free Printable Documents Late Rent Notice Rental Property Management Rent

Printable Sales Contract For Buying Subject To Template 2015 Real Estate Contract Real Estate Forms Contract Template

To Know The Tax Benefits Provided To First Time Home Buyers Watch Out Image Below To Grab These Benefits Just Call Out 8852 Finance Loans Loan Investing

Free Offer To Purchase Real Estate Pro Buyer Form Wholesale Real Estate Real Estate Forms Real Estate Contract

Final Rules On Fiduciary Fees Are Issued Accounting Programs Estate Tax Tax Deductions

The regulations apply to tax years beginning on or after jan.

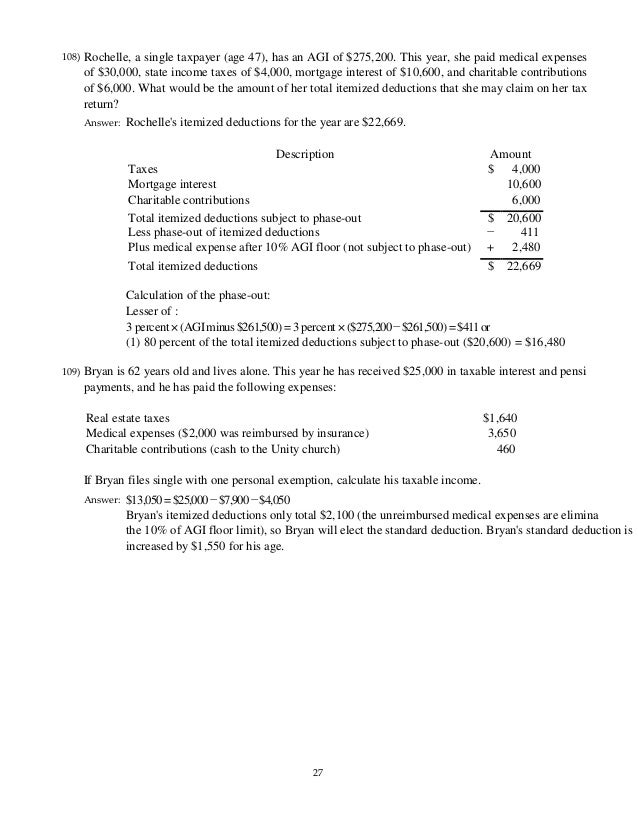

Estate deductions subject to 2 floor. Examples of itemized deductions not subject to the 2 floor include costs related to fiduciary income tax returns and estate tax returns probate court costs and certain appraisal fees. E read as follows. These regulations which are essentially unchanged from the much maligned proposed regulations first issued in 2007 govern trust and estate costs subject to the 2 percent floor on miscellaneous itemized deductions. 642 h provided that in the year of termination of a trust or estate any excess deductions claimed under either 67 b or 67 e should be passed to the beneficiaries and were considered 67 b miscellaneous itemized deductions subject to the 2 agi limitation.

Deductions for attorney accountant and preparer fees are limited on schedule a of form 1040. Report other miscellaneous itemized deductions on form 1041. Miscellaneous itemized deductions are those deductions that would have been subject to the 2 of adjusted gross income limitation. You can still claim certain expenses as itemized deductions on schedule a form 1040 1040 sr or 1040 nr or as an adjustment to income on form 1040 or 1040 sr.

To figure the amount of your allowable deduction for these expenses the irs provides a section on schedule a job expenses and certain miscellaneous deductions. When filing form 1040 or form 1041 for a decedent estate or trust you must determine how to deduct administration fees. Under the internal revenue code miscellaneous itemized deductions are allowed for individuals which include trusts and estates only to the extent that the aggregate deductions exceed 2 percent of adjusted gross income. Deductions in excess of income in the final year of a trust or estate pass through to beneficiaries as miscellaneous itemized deductions even if the expenses would otherwise be characterized as itemized.

Many of these deductions will be subject to the 2 percent. For purposes of this section the adjusted gross income of an estate or trust shall be computed in the same manner as in the case of an individual except that the deductions for costs which are paid or incurred in connection with the administration of the estate or trust and would not have been incurred if the property were not held in such trust or estate shall be. However certain expenses of an estate or trust are not subject to the 2 percent floor. Although notice 2018 61 allows estates and trusts to continue to take deductions for administration expenses that would not have been incurred if the property were not held in the estate or trust the first category of expenses not subject to the 2 floor the notice does not say whether beneficiaries may take deductions for those expenses when an estate or trust terminates.

Acct 426 Tax I Chapter 10 Flashcards Quizlet

Month To Months Residential Rental Agreement Free Printable Pdf Format Form Rental Agreement Templates Lease Agreement Free Printable Room Rental Agreement

Offer Letter Format In Word In 2020 Letter Format Sample Letter Templates Free Lettering

Subject To Existing Liens Aka Sub 2 Real Estate Contract Download Now Real Estate Contract Real Estate Investing Positive Cash Flow

Available Homes Mcguinn Homes New Homes In Columbia Sc Publisher Clearing House Home Buying Home

Taxation Of Individuals And Business Entities 2018 Edition 9th Editio

Personal Assistant Agreement Best Of 32 Sample Contract Templates In Microsoft Word Peterainsworth In 2020 Contract Template Contract Templates

Printable Sample Free Printable Rental Agreements Form Lease Agreement Rental Agreement Templates Room Rental Agreement

Home Improvement Contractia Requirements Sample Nyc Template New York In Photos Hd Didierrecl Construction Contract Roofing Contract Residential Construction

Driving The Same Car For Business And Personal Use Photography Business Tips Articles Photography Office Tax Preparation Quotes About Photography

Mending The Piggy Bank Budgeting Spreadsheet Budget Spreadsheet Budgeting Spreadsheet

Tax Time Tax Time Home Business Business Magazine

Buffer A Smarter Way To Share On Social Media Backyard Views Garage Style Backyard

New Irs Regulations Regarding Trust And Estate Costs And Expenses Fiskeco Com Fiskeco Com

Pergola Front Porch In 2020 Pergola House Styles Front Porch

The Cost Per Unit Of Keeping Your Home Warm The Unit Home Com Home Schooling

Million Mansion That Is Still On The Market Photos And Premium High Res Pictures Stone Mansion Mansions Exterior

On Valentine 039 S Every Other Day We Love Lawsuits Infographic In Law Suite Legal Nurse Consultant Infographic

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcqcdbqvym69vi4utfsvxea881toz9v0klyqhcahwzdcifur8gfq Usqp Cau

709 S Walnut Street Floor Trim Marysville Hardwood Floors

House Warming Gift Artwork From A Photo In Pen Ink From Giveamasterpiece Com House Portraits Custom House Portrait Photo Art Gallery

50 Cent Battles In Bankruptcy Court To Save His Connecticut Mention Former Home Of Iron Mike Tyson Is Subject In 50 Cent Mike Tyson 50 Cent House Poplar Hill

Open House Welcome Sign No 2 Open House Real Estate Real Estate Signs Open House Signs

Custom Testimonial Prop Home Buying Tips Real Estate Tips Real Estate Signs

What Home Buyers Need To Know When Mortgage Rates Rise Even Just A Fraction Mortgage Rates Best Mortgage Lenders Mortgage

Sometimes Something Might Appear Expensive But It Always Depends What You Get In Return Therefore Don T Think Real Estate Financial Modeling Excel

Buying V Renting For Long Term Responsibility Infographic Retirement Advice Real Estate Tips Real Estate Buying

5 Bedrooms Detached Duplex For Sales At Magodo Lagos Sale House Duplex For Sale House

30 Day Notice To Vacate Letter Real Estate Forms Being A Landlord Lettering Real Estate Forms

Personal Property Rental Agreement Forms Property Rentals Direct Termination Of Lease Agr Lease Agreement Rental Agreement Templates Termination Of Tenancy

2 Floor Itemized Deductions Employee Expenses Trump Tax Reform

If You Think Have To Choose Between Being Eco Friendly And A Good Budget Think Again With These Energy Saving Hacks You Real Estate Home Living Room Designs

Living Room Kitchen Floor Transition Livingroomideas Floor Kitchen Living Livingroomideas Room Transition In 2020 Home Hanging Curtains Home Decor

Posted Byu Retro1123 No Spoilers Playing A Cleric Of Matt Mercer In Dragon Heist Dm Just Sent Me This Critical Role Dungeons And Dragons Mercer

Ultimate Home Inspection Checklist Real Estate Home Buyer Etsy In 2020 House Hunting Checklist Inspection Checklist Real Estate Tips

Price Drop Amenity Rich Gated Heritage Harbor In The Steinbrenner Martinez Mckittrick School District Built In Desk Home Office Space Great Rooms

Calif Property Taxes Are Due Income Tax Filing Taxes Accounting Services

Download Free Homeland V3 0 7 Responsive Real Estate Theme For Wordpress Direct Download Link Http Nulledgraphic C Real Estate Wordpress Real Estate Houses

Termination Of Lease Agreement Form Free Printable Documents Lease Agreement Rental Agreement Templates Termination Of Tenancy

Free Printable Rental Agreement Elegant 11 Best Rental Agreements Images On Pinterest Rental Agreement Templates Lease Agreement Room Rental Agreement

Unique Rental Application Form Free Xls Xlsformat Xlstemplates Xlstemplate Check More At H Rental Agreement Templates Lease Agreement Room Rental Agreement

Of The Day Quest Latest Finance And Credit Hacks Blogging Fusion Blog Directory In 2020 Improve Your Credit Score Credit Bureaus Credit Solutions